Analysis of Sabka Vishwas

(Legacy Dispute Resolution)

Scheme, 2019

|

One of the flagship agenda of the present Government is to create an ease of doing business in our country. The purpose of creating an ease in doing business is to boost the investment and in turn growth rate for the country. Several reforms undertaken in line with the stated policy led to India jumping the rank in the World Bank’s Ease of Doing Business by 23 places to 77 amongst 190 nations. India is in fact the only country to rank among the top 10 improvers for the second consecutive year. One area however that remains as a bottleneck in creating the ease for existing businesses is the quantum of legacy disputes in indirect taxation which are pending at various stages. It has been estimated that nearly INR 3.75 lakh crores are involved due to disputes pending resolution under legacy indirect taxation system (viz., Central Excise & Service Tax). Hence to move past the said disputes by resolving the same, Hon. Finance Minister of India announced SABKA VISHWAS (LEGACY DISPUTE RESOLUTION) SCHEME, 2019 (hereinafter referred as “scheme”) as part of the Budget Proposal in July 2019. Hon. Minister had this to say on the floor of the Parliament while proposing the scheme:

“GST has just completed two years. An area that concerns me is that we have huge pending litigations from pre-GST regime. More than 3.75 lakh crore is blocked in litigations in service tax and excise. There is a need to unload this baggage and allow business to move on. I, therefore, propose, a Legacy Dispute Resolution Scheme that will allow quick closure of these litigations. I would urge the trade and business to avail this opportunity and be free from legacy litigations.”

Hence the aim as apparent from the above extract is to unload the baggage by allowing the businessmen to close the pending litigations and to move forward. On merits the intent of the Government is laudable and hence advisable for the businessmen to take advantage of the same, wherever found fit. However for deciding whether to opt for the scheme or not the businessmen (with the help of professional) would essentially be required to consider the probable outcome of the dispute, if continued, vis-à-vis resolving the same under the scheme considering the merits and the quantum of each case individually. It may be noted that the success rate of department in higher appeals is very miserable. A win in appeal will give full relief from the tax dues whereas the declaration under the scheme will not give total relief from the tax dues.

Scheme also permits voluntary disclosure and provides certain reliefs in this regard. Hence it would be correct to say that the scheme not only resolves the disputes but also provides for an opportunity to declare the unpaid dues and avail the relief.

Said scheme has been formulated by way of Chapter V of the Finance Act (No. 2), 2019 (hereinafter referred as “Act”). Rules, circulars & FAQ’s have been issued to provide for the procedural aspects/clarifications related to the scheme. Provisions of the Act along with related rules and clarifications are referred at appropriate places in the present book to enable proper understanding of the scheme.

Department is also keen to ensure the success of the scheme as evident from paragraphs 2 & 12 of circular No. 1071/4/2019-CX.8 dt. 27.08.2019 which urges the departmental officers to partner with the trade and industry and help to make the scheme a grand success.

Further paragraph 11 of the said circular also provides the directions to be followed by the department to free the taxpayers from the burden of legacy disputes by popularizing the scheme and enabling smooth execution.

From the reading of scheme it would appear that the same is very generous as relief even with respect to the tax amount is granted. Also the department is keen to make it a success. Therefore the benefit of the scheme must be availed after assessing the merits of each case.

The book examines the provisions of the scheme in detail in the Q & A format for easy understanding. Same shall also aid in resolving specific queries of the readers by reaching to the conclusion swiftly as opposed to reading the entire book although we would urge for full reading of the book to understand all the contours of the scheme. Let us start the exploration.

Notes on the clauses in the Finance Bill (No. 2), 2019 dealing with the provisions of the scheme reads as under:

“The Scheme is one time measure for liquidation of past disputes of Central Excise and Service Tax as well as to ensure disclosure of unpaid taxes by a person eligible to make a declaration. The Scheme shall be enforced by the Central Government from a date to be notified. It provides that eligible persons shall declare the tax dues and pay the same in accordance with the provisions of the Scheme. It further provides for certain immunities including penalty, interest or any other proceedings under the Central Excise Act, 1944 or Chapter V of the Finance Act, 1944 to those persons who pay the declared tax dues.”

Hence the scheme has twin purposes of -

- settling the disputes and

- enabling voluntary disclosure of unpaid taxes to non-compliant taxpayers.

Scheme offers lucrative reliefs to achieve the above stated objectives.

The scheme not only aims to settle the legacy disputes by granting amnesty from partial tax dues, interest, penalty as well as prosecution but also provides for a voluntary declaration granting amnesty from interest, penalty as well as prosecution in this regard. The honest taxpayers would naturally feel that they have been treated unfairly as they would have ended up paying the due tax along with interest and penalties and now the dishonest taxpayers would get the relief. Hence a question would arise as to whether such scheme can be held to be valid considering that Article 14 of the Constitution of India grants equality before the law to every person and therefore a dishonest person cannot be treated favourably.

Before we discuss the legal precedents on the issue, it is worthwhile to note that the scheme has a much larger goal of settling the legacy disputes for smooth implementation of GST. Settling of the disputes would be not only in the interest of trade but even in the interest of the Government as it would remove the uncertainty associated with it. A prudent businessmen as well as forward looking Government would always prefer to remove the uncertainties by proposing a solution fair to both the sides. Hence it can be contended that in such situations (and they are many) the scheme shall pass the moral test of fairness. Therefore an honest tax payer need not be disheartened by such scheme as it serves a much larger purpose of removing the uncertainties and not granting any unfair benefit. Said contention would also draw support from the fact that litigants pursuing justice on an issue backed by clear language of law or legal precedents would not like to make a declaration under the scheme but on the other hand would continue to pursue the litigation for lack of any uncertainty in such cases.

Now let us refer to some legal precedents on the issue of constitutional validity of such schemes. In 1981, Special Bearer Bonds (Immunities and Exemptions) Ordinance, 1981 was issued by the President (later replaced by an Act) to permit the Central Government to issue special bonds wherein it would be possible for persons in possession of black money to invest the same in the said Bonds. It allowed full protection to such persons from any inquiry or investigation pertaining to the black money invested in such bonds. Validity of the said Ordinance along with the Act (which replaced the Ordinance) was challenged before the Supreme Court in the case of R.K. Garg v. Union of India [1981] 7 Taxman 53 (SC) on the ground that it violates Article 14 of the Constitution of India. Supreme Court upheld the validity of the Ordinance as well as the Act by observing the following:

“The object of the Act being to unearth black money for being utilised for productive purposes with a view to ensuring effective social and economic planning, there had necessarily to be a classification between persons possessing black money and others and such classification could not be regarded as arbitrary or irrational.”

On the issue of whether the aspect of morality is relevant, Supreme Court observed as under:

“Morality can in no case have relevance to the constitutional validity of a legislation. There may be cases where the provisions of a statute may be so reeking with immorality that the legislation can be readily condemned as arbitrary or irrational and hence violative of article 14. But the test in every such case would be not whether the provisions of the statute offend against morality but whether they are arbitrary and irrational having regard to all the facts and circumstances of the case. Immorality by itself is not a ground of constitutional challenge and it obviously cannot be, because morality is essentially a subjective value, except insofar as it may be reflected in any provision of the Constitution or may have crystallised into some well-accepted norm of special behaviour. Hence, it could not be contended that the Act was unconstitutional on the ground that it offended against morality by according, to dishonest assessees, who had evaded payment of tax, immunities and exemptions which were denied to honest taxpayers.”

Also in 1997, Government of India came out with VDIS under the direct taxes. Said scheme permitted voluntary disclosure of unaccounted income and granted several reliefs in terms of tax, interest, penalty as well as prosecution. Said scheme was challenged before the Bombay High Court in the case of All India Federation of Tax Practitioners v. UOI [1997] 93 Taxman 737 (Bombay) on several grounds including the ground that it rewards dishonest tax payers and is also not designed based on intelligible differentia and hence violates Article 14 of the Constitution of India. The Court upheld the validity of the scheme essentially on the ground that the formulation of a scheme is a policy decision of the Parliament and the Court would have very limited jurisdiction going into such policy matters. Said judgment was subsequently also upheld by the Supreme Court ([1998] 231 ITR 24 (SC)).

The Courts may declare the scheme as unconstitutional, only when it is arbitrary and irrational having regard to all the facts and circumstances of the case and not merely on the ground that it may subjectively look immoral to some tax payers. Also Courts would be reluctant to go into the details of the scheme, as it is a policy decision of the legislature, if on an overall basis there is a justification for introducing such schemes.

Thus it appears that the present scheme has spelled out the reasoning for its requirement (dispute resolution + voluntary disclosure to move past legacy taxation) and hence should pass the test of validity based on the above cited precedents.

However there are certain aspects of the scheme which may require to be tested on the pedestal of Article 14. Such aspects are discussed at appropriate places in this book.

Sec. 120(2) of the Act provides that the scheme shall come into force on such date as the Central Government may, by notification in the Official Gazette, appoint.

Hence by exercising the said power, Government has issued Notification No. 04/2019 Central Excise-NT dt. 21.08.2019 appointing 1st of September, 2019 as the date from which the scheme shall be operational.

Act does not contain any end date till when the scheme shall remain operational. However Sec. 132(1) & (2) of the Act grants the power to the Government to make rules for carrying out the provisions of the scheme. Accordingly by exercising the said powers, Notification No. 05/2019 Central Excise-NT dt. 21.08.2019 has been issued to provide for the Sabka Vishwas (Legacy Dispute Resolution) Scheme Rules, 2019 (hereinafter referred as Rules). As per Rule 3(1) of the said Rules, the declaration to be made under the scheme shall be made electronically at https://cbic-gst.gov.in in Form SVLDRS-1 by the declarant, on or before the 31st December, 2019. Hence the end date for making the declaration under the scheme shall be 31st December, 2019.

The end date of 31st December, 2019 is not for making the payment under the scheme or for issuance of discharge certificate. It is only the end date for making a declaration under the scheme.

Before discussing different aspects of the scheme threadbare, it is worthwhile to consider the underlying structure of the provisions contained in the Act related to the scheme. Following table can hence act as a reference point for all the discussions done henceforth:

|

Relevant Section

|

Brief Content

|

|

120

|

Short title of the scheme and commencement.

|

|

121

|

Provides for the definitions of certain terms used in the scheme.

|

|

122

|

Provides for the various indirect tax enactments in respect of which declaration can be made under the scheme.

|

|

123

|

Provides for the definition of “tax dues” which can be declared under the scheme.

|

|

124

|

Provides for the relief available under the scheme with respect to the “tax dues” declared.

|

|

125

|

Provides for the persons who are eligible to make the declaration under the scheme as well as the manner of declaration.

|

|

126

|

Provides for the verification of the declaration by the designated committee.

|

|

127

|

Provides for issuance of the statement of amount payable as well as discharge certificate by the designated committee.

|

|

128

|

Provides for the rectification of the statement of amount payable issued by the designated committee.

|

|

129

|

Provides for the issuance of the discharge certificate.

|

|

130

|

Provides for certain restrictions under the scheme relating to payment of tax dues declared, claim of credit thereof as well as refund.

|

|

131

|

Provides for removal of doubts relating to the benefit, concession or immunity granted under the scheme.

|

|

132

|

Provides for the power of the Government to make rules.

|

|

133

|

Provides for the power of the CBIC to issue orders, instructions, etc.

|

|

134

|

Provides for the removal of difficulties by issuance of order by the Government.

|

|

135

|

Provides for certain protection to the officers.

|

Sec. 122 of the Act provides that the scheme shall be applicable to the dues under the following enactments:

|

ENACTMENT

|

NATURE

|

|

Central Excise Act, 1944 or the Central Excise Tariff Act, 1985 and the rules made thereunder.

|

Excise Duty

|

|

Chapter V of the Finance Act, 1994

|

Service Tax

|

|

Agricultural Produce Cess Act, 1940

|

Cess

|

|

Coffee Act, 1942

|

Excise Duty

|

|

Mica Mines Labour Welfare Fund Act, 1946

|

Cess

|

|

Rubber Act, 1947

|

Excise Duty

|

|

Salt Cess Act, 1953

|

Cess

|

|

Medicinal and Toilet Preparations (Excise Duties) Act, 1955

|

Excise Duty

|

|

Additional Duties of Excise (Goods of Special Importance) Act, 1957

|

Excise Duty

|

|

Mineral Products (Additional Duties of Excise and Customs) Act, 1958

|

Excise Duty

|

|

Sugar (Special Excise Duty) Act, 1959

|

Excise Duty

|

|

Textiles Committee Act, 1963

|

Cess

|

|

Produce Cess Act, 1966

|

Cess

|

|

Limestone and Dolomite Mines Labour Welfare Fund Act, 1972

|

Cess

|

|

Coal Mines (Conservation and Development) Act, 1974

|

Excise Duty

|

|

Oil Industry (Development) Act, 1974

|

Excise Duty

|

|

Tobacco Cess Act, 1975

|

Cess

|

|

Iron Ore Mines, Manganese Ore Mines and Chrome Ore Mines Labour Welfare Cess Act, 1976

|

Excise Duty/Cess

|

|

Bidi Workers Welfare Cess Act, 1976

|

Cess

|

|

Additional Duties of Excise (Textiles and Textile Articles) Act, 1978

|

Excise Duty

|

|

Sugar Cess Act, 1982

|

Cess

|

|

Jute Manufacturers Cess Act, 1983

|

Cess

|

|

Agricultural and Processed Food Products Export Cess Act, 1985

|

Cess

|

|

Spices Cess Act, 1986

|

Cess

|

|

Finance Act, 2004

|

Cess

|

|

Finance Act, 2007

|

Cess

|

|

Finance Act, 2015

|

Cess

|

|

Finance Act, 2016

|

Cess

|

|

Any other Act, as the Central Government may, by notification in the Official Gazette, specify

|

-

|

Dues arising under the CENVAT Credit Rules, 2004 will also be covered under the scheme as the said rules have been made by exercising the powers granted by section 37 of the Central Excise Act, 1944 as well as section 94 of the Finance Act, 1994.

Here it may be noted that even the Finance Act, 2004, the Finance Act, 2007, the Finance Act, 2015 & the Finance Act, 2016 have been included so as to cover under the scheme dues with respect to various cesses (Education cess, Secondary and higher education cess, Swachh Bharat cess & Krishi Kalyan cess).

Sec. 122(c) of the Act grants power to the Central Government to specify by way of issuance of notification any other Act which can be covered under the scheme. No such notification has been issued till now and hence only the enactments given supra are covered under the scheme.

Tax disputes under following enactments are not covered under the scheme:

|

Customs Act, 1962 or the Customs Tariff Act, 1975

|

|

State legislations such as VAT, Entry Tax, Octroi, Luxury Tax, Entertainment Tax, etc.

|

|

Central Sales Tax Act, 1956

|

|

Goods and Services Tax Act’s (GST)

|

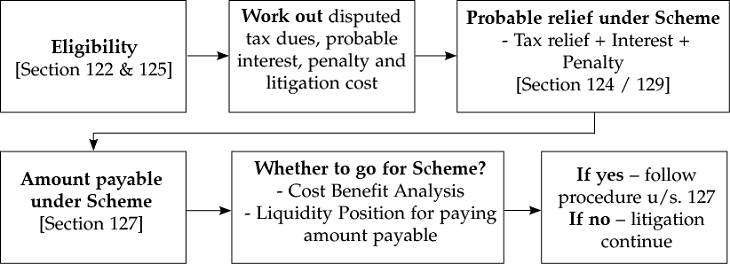

Broad perusal of the scheme structure would entail that to understand and apply the scheme, one needs to first obtain the details of the dues under the indirect tax enactments of the person in question. One has to then evaluate the merits of the dues. All the pending cases of a person in question may be divided into two broad categories viz. Strong case and unpredictable case based on following parameters:

Strong case

- Favourable retrospective amendment in the Act

- Subsequent favourable notification / clarification / circular

- Matters settled by Tribunal / High Court / Supreme Court

- Demand arisen out of mis-comprehension of facts and arithmetical errors

- Time-barred demands

- Frivolous demands

Unpredictable case

- Where two interpretations are possible on issue involved

- Absence of clarification from department on legal position

- No settled jurisprudence

- Difference in view between two or more High Courts or Tribunals

- Issue pending before Hon’ble Supreme Court

- Facts do not support the strong legal contentions

Once the cases are bifurcated as above, in unpredictable cases the scheme may be explored considering the cost benefit analysis, risk appetite and liquidity position. For strong cases the benefit may be availed if stake is nominal and litigation hassles and costs are high.

In nutshell, if assessee is uncertain about a particular legal position taken by him and expects liabilities on losing the case, it would be prudent to apply under the scheme then to be brave and assume the risk of uncertainty.

Decision making flow-chart can be as under:

We suggest to adopt the above described thought process while dealing with the scheme to facilitate its application to actual cases.

Sec. 125(1) of the Act provides that all persons shall be eligible to make a declaration under the Scheme barring few exceptions.

Further the word “person” has been defined u/s. 121(q) of the Act to include every kind of assessee. Hence every kind of assessee can make a declaration under the scheme subject to certain restrictions (discussed later). Also it is not necessary that the person intending to make a declaration under the scheme needs to have been registered at the relevant time under the enactments for which dues are being declared. Hence even an unregistered person can make the declaration.

The word “declarant” has been defined u/s. 121(h) of the Act to mean a person who is eligible to make a declaration and files such declaration under section 125. Thus a person eligible to make a declaration under the scheme and who in fact makes the declaration shall be considered as a “declarant”.

Following table summarizes the categories under which declaration can be made under the scheme:

|

CATEGORY

|

SUB-CATEGORY

|

|

Litigation

|

Show-cause notices pending as on 30.06.2019

|

|

Appeals pending as on 30.06.2019

|

|

Enquiry, investigation or audit

|

Enquiry or investigation in respect of which dues have been quantified as on 30.06.2019

|

|

Audit in respect of which dues have been quantified as on 30.06.2019

|

|

Amount in arrears

|

Admitted liability in returns filed on or before 30.06.2019

|

| |

Appeal not filed or appeal having attained finality

|

|

Voluntary Disclosure

|

—

|

Clauses (a) to (h) of Sec. 125(1) of the Act provides for certain restrictions as regards the persons who can make the declaration under the scheme. Restrictions and banned cases under each category are as under:

|

CATEGORY

|

RESTRICTIONS

|

RELEVANT SECTION

|

|

Litigation

|

Appeal which has been heard finally on or before 30.06.2019

|

125(1)(a)

|

|

Show Cause Notice issued and final hearing has taken place on or before 30.06.2019

|

125(1)(c)

|

|

Show Cause Notice has been issued for refund or erroneous refund

|

125(1)(d)

|

|

Application before Settlement Commission is made

|

125(1)(g)

|

|

Enquiry, investigation or audit

|

Person subjected to audit, investigation or enquiry where quantification is not made on or before 30.06.2019

|

125(1)(e)

|

|

Amount in Arrears

|

No restrictions

|

-

|

|

Voluntary Disclosure

|

Voluntary Disclosure cannot be made by a person (i) after being subjected to any enquiry, audit or investigation or (ii) Return filed and amount is indicated as payable but has not been paid

|

125(1)(f)

|

In addition to the above restrictions, following additional restrictions shall apply across all the categories described above:

- Person who have been convicted for any offence for the matter cannot make a declaration on such matter (Sec. 125(1)(b)).

- Person cannot make declaration with respect to the excisable goods set forth in the Fourth Schedule to the Central Excise Act, 1944 (125(1)(h)) viz., Tobacco and Manufactured Tobacco substitutes and Petroleum products.

It may happen that a person may be restricted from making a declaration under a particular category. For example, a person has an appeal pending and the final hearing of the same has been done on or before 30th June, 2019. Hence such person is restricted from making a declaration u/s. 125(1)(a) of the Act. Now let us say such person has received an order on 15th July, 2019 wherein the dues stands recoverable. Thus the said dues would fall within the definition of “amount in arrears” u/s. 121(c) if such person does not intend to litigate the case further. Hence the issue before us is whether such person can seek relief under the category of “amount in arrears” when he is debarred under the category of “litigation”?

It may be noted that the provisions of the Act do not provide that the categories under which declaration can be made are mutually exclusive. Hence a debarment under a particular category would not result in debarment under the other category, if the said other category does not restrict making of the declaration.

Said view is also supported by Table No. 8 of the declaration form SVLDRS-1 wherein the restrictions are clearly applied qua the category and not qua the entire scheme.

This position is amply clarified by para no. 2(vii) and 2(viii) of Circular no. 1072/05/2019 – CX dt. 25.09.2019.

Thus in the given example, the “amount in arrears” category will be available to the person in question even if such person is restricted from making a declaration under the “litigation category”.

There is a possibility that SCN was pending as on 30th June, 2019 but same has been adjudicated on or after 01st July, 2019. The said adjudication order attained the finality on or before 31st December 2019. In given case, assessee falls under “litigation” category as SCN was pending as on 30th June, 2019 and also falls under “amount in arrears” category. The issue here is whether declarant has a choice to decide the category under which declaration can be filed. If he goes for litigation category relief is higher than amount in arrears category.

Act does not expressly provide for such situation. One may take the position that he is entitled to opt for the most beneficial category.

It may also happen that a person in question may be ineligible to file the declaration under any one of the clauses contained u/s. 125(1). As an example a person in question might have been issued a show cause notice under indirect tax enactment for an erroneous refund or refund. Now as per Sec. 125(1)(d) of the Act, such “person” is not eligible to file a declaration under the scheme. Whether this would mean that such person cannot even file a declaration in respect of other show cause notices or appeals for which he is otherwise eligible? In other words, are the restrictions given u/s. 125(1) of the Act qua the person or qua the case?

Now restriction u/s. 125(1)(b) of the Act pertaining to the person who have been convicted for any offence punishable under any provision of the indirect tax enactment for a matter clearly provides that the said restriction is only with respect to the said matter and not for other matters. However other clauses u/s. 125(1) do not provide for such language.

Circular No. 1071/4/2019-CX.8 dt. 27.08.2019 however beneficially clarifies as under:

“(b) Section 125(1)(d) mentions that the Scheme is not available to an applicant who has been issued a show cause notice relating to refund or erroneous refund. It has potential to lead to an interpretation that such persons will not be able to opt for the Scheme for any other dispute as well, since the restriction is on ‘the person’ in place of ‘the case’. It is clarified that the exception from eligibility is for ‘the case’ and not ‘the person’. In other words, if a person has been issued a show cause notice for a refund/erroneous refund and, at the same time, he also has other outstanding disputes which are covered under this Scheme, then, he will be eligible to file a declaration(s) for the other case(s). Same position will apply to persons covered under Sections 125(1)(a), (b), (c), (e) and (g).”

Above clarification thus provides that the restrictions contained u/s. 125 shall be read as qua the case and not qua the person. Clause (f) of Sec. 125 do not permit a person to make a voluntary disclosure in certain scenario (discussed later in the book). He would not be debarred from making a declaration under other clauses. Similarly clause (h) restricts the person from making a declaration pertaining to excisable goods set in fourth schedule (petroleum products & tobacco). However, such person would not be debarred from making a declaration under other clauses for goods not covered by the fourth schedule.

Are not are the above clarifications going beyond the provisions of the Act? Can the word “person” used in Sec. 125(1) be read as a “case” as sought by the circular?

The word “person” can indeed be read as “case”. There could be two plausible explanations in this regard. Even though the definition of “person” u/s. 121(q) provides for the legal entity in question and not the case as a person, still the said definition is subject to first line in Sec. 121 of the Act which reads as under:

“Sec. 121. In this Scheme, unless the context otherwise requires,—“

Thus the definitions given under the said Sec. 121 can be departed with if the context requires otherwise. The scheme if seen in entirety operates case-wise. The declaration under the scheme as well as reliefs, benefits, immunities and restrictions are qua the case. In such scenario it becomes inevitable that the restrictions given u/s 125(1) are also to be read case-wise. This is what the circular does. Hence there seems to be no infirmity in the said circular.

Second explanation is that the power granted to the Board u/s 133 of the Act can be exercised to tone down the rigour of the law by way of an executive action. The legality of the same has been upheld by Supreme Court in the case State Bank of Travancore v. CIT [1986] 158 ITR 102 (SC). For detailed discussion on this please refer to the question in this book related to the powers granted to the Board to issue such circulars.

Sec. 125(1)(a) of the Act provides that the person who has filed an appeal before the appellate forum and such appeal has been heard finally on or before the 30th day of June, 2019, such person cannot make a declaration under the litigation category.

The term “appeal” has not been defined in the Act. However the said term has been used in conjunction with the term “appellate forum”. The term “appellate forum” has been defined u/s. 121(f) of the Act as follows:

“(f) “appellate forum” means the Supreme Court or the High Court or the Customs, Excise and Service Tax Appellate Tribunal or the Commissioner (Appeals)”

Hence the term “appeal before the appellate forum” would mean the appeals filed before the Supreme Court or the High Court or CESTAT or the Commissioner (Appeals).

The issue however will arise as to whether the cases wherein writs have been filed before the High Courts or Supreme Courts would also be considered under the term “appeal” or only the tax appeals filed under the express provisions of law would only be considered ?

To resolve the issue one needs to consider Sec. 127(7) of the Act dealing with the issuance of discharge certificate. It provides that if the declaration is pertaining to the tax dues in respect of which any writ petition or reference has been filed before the High Court or the Supreme Court against any order, the declarant must withdraw the same and furnish the proof along with the proof of payment to obtain the discharge certificate. Hence clearly the intent is to cover writs as well as reference, pending before the High Court or Supreme Court, under the scheme provided said matters have not been heard finally on or before 30th June, 2019.

Now the term “appeal has been heard finally” has not been defined in the Act. The word “final” has been held to be last; that which absolutely ends (38 Mad 41). Ballentine’s Law Dictionary has defined the word “final hearing” as the hearing which results in a final decision or the adjudication.

It has been held under the Code of Civil Procedure that the word “hearing” would mean all the stages of a trial including taking the evidence, hearing the arguments, other proceedings till the final adjudication of the suit (see Kanaran Nambiar v. Ramunni Nambiar (AIR 1961 Ker 290)). Hence the word “hearing” would imply not only the oral hearing but even the opportunity granted to make written submissions in connection with the given proceedings. Having said that, the term “final hearing” would then mean the last opportunity exercised by the assessee to make a representation (oral or written) concerning the case.

The determination of whether appeal has been heard finally or not on or before 30th June, 2019 is a question of fact. One way to determine whether the hearing was final or not is whether the pronouncement of order takes place without any more submissions/hearings. If the answer is yes, the hearing can be said to be final. In cases pending before CESTAT, the status of appeal can be viewed on the portal and hence cases where the hearings have happened on or before 30th June, 2019 and only pronouncement of order is pending would also be considered as heard finally, provided such cases are not reheard. In all other cases, the factum of final hearing needs to be ascertained.

In cases where oral hearing has taken place on or before 30th June, 2019 but the assessee has requested to make an additional submission and such submission is made on or after 1st July, 2019, it can be contended that “final hearing” has not taken place on or before 30th June, 2019.

Also cases where the appeals have not yet been decided and the appellant desires to make an additional submission, such permission cannot be denied in the interest of natural justice. In such situations also where additional submissions are made on or after 1st July, 2019 it can be contended that the final hearing has not taken place on or before 30th June, 2019 so as to be covered by restriction u/s. 125(1)(a).

It may also happen that the hearing (already concluded) for a case may be called for rehearing due to new bench, change in officer or any other reason. In this case it cannot be said that final hearing has taken place and hence the restriction would not apply. Paragraph no. 10(e) of Circular No. 1071/4/2019-CX.8 dt. 27.08.2019 also confirms the said view.

It may happen that a person might have filed an appeal on or before 30th June, 2019 but the same might not have been admitted by the said date due to reasons such as belated filing with an application to condone the delay, short payment of pre-deposit, etc. Can such declarant claim the relief discussed above u/s 124(1)(a) under litigation category ?

It may be noted that Sec. 124(1)(a) grants relief in cases where appeal is pending as on 30th June, 2019. Said provision does not expressly provide that the said appeal needs to be admitted by the said date.

Reference here may also be made to the decision of Madras High Court in the case of State of Tamil Nadu v. K. Damodarasamy Naidu & Bros (2007) 10 VST 716 (Mad). In the said case similar issue arose in the context of Settlement of Disputes Act. It was held that when the terminology employed in the section is “pending”, it is impermissible to import any additional word in the provision that in order to be eligible to make an application, the appeal must be admitted as the word “admission” has not been used. Hence it can be contended that even appeals pending admittance can claim relief u/s. 124(1)(a).

Sec. 125(1)(a) does not restrict cases where appeal is pending as on 30th June, 2019 (except when heard finally). Said provision does not expressly provide that the cases where defect memo are issued on or after 1st July, 2019 are outside its ambit.

Reference here may also be made to the decision of Andhra Pradesh High Court in the case of Senate Fashions v. Deputy Commissioner (2002) 128 STC 89 (AP). In the said case an objection was raised as to the pagination of the appeal filed before the stipulated date. Benefit of the settlement scheme was sought to be denied on the ground that such appeal cannot be considered as pending. High Court allowing the petition held that even the appeals filed before the stipulated date has to be considered as pending despite the fact that certain objections might have been raised by the registry after the stipulated date in the context of such appeal.

There can be situations wherein the appeals filed have been heard finally on or before 30th June, 2019 and hence gets covered by the restrictions given u/s. 125(1)(a) discussed earlier. Hence apparently such person cannot make the declaration in respect of tax dues. What is the recourse available to such person?

Let us first consider a situation wherein appeal has been heard finally but the order has not been issued till date. There is a possibility of withdrawing the said pending appeal. This is because the dues emanating out of an order pending in appeal would take the colour of “amount in arrears” if the appeal is withdrawn. In such eventuality declaration can be made under the “amount in arrears” category which we shall discuss later.

Let us also consider another scenario wherein the appeal filed has been heard finally on or before 30th June, 2019 and the order has also been passed on or after 1st July, 2019 but before the last date for making the declaration under the scheme (i.e. 31st December, 2019). Such case could be considered as “amount in arrears” and declaration under the said category can also be made. Please refer the detailed discussion on the said issue later.

Reliance is placed on the decision of Padiyur Sarvodaya Sangh v. CCE (2008 (227) E.L.T. 441 (Tri. - Chennai) wherein the appellant sought restoration of appeal withdrawn earlier due to an erroneous consideration of a notification. Tribunal held as under with respect to its power to enable withdrawal as well as restoration of appeal:

“3. After giving careful consideration to the submissions, we are inclined to accept the proposition that, if this Tribunal has power to allow an application for withdrawal of appeal, it also has the power to allow, on sufficient grounds, an application for withdrawal of such an application. Rule 41 enables this Tribunal to pass such orders or issue such directions as may be necessary to meet the ends of justice in a given case.”

One may also refer to the decision of Gujarat High Court in the case of Gayatri Enterprise v. State of Gujarat 2017 (6) G.S.T.L. 392 (Guj.) wherein the petitioner initially withdrew the appeal pending before the Tribunal to take the benefit of amnesty scheme. Subsequently the benefit was denied on some other grounds and hence the petitioner sought restoration of the said appeal before the Tribunal. Tribunal rejected the restoration application on the ground that the appeal was withdrawn unconditionally. High Court allowed the restoration and held as under:

“The Tribunal in exercise of its discretion ought to have permitted revival of the petitioner’s Second Appeals namely Second Appeals No. 891 of 2013 and 892 of 2013, in view of the fact that the withdrawal was only prompted as it was so required. In order to get the benefit of the Scheme, the appeals had to be withdrawn. Once the benefit was such a scheme was not extended, the withdrawal was rendered of no use. Appeals therefore needed to be restored and heard on merits. In our opinion merely because the orders permitting withdrawal of appeals did not contain an observation of liberty to revive would not disentitle the petitioner of the same benefit of revival of the Appeals.”

Reference here can also be made to number of directions issued by the Board from time-to-time directing the department to withdraw the appeal either due to monetary limits or due to issue being settled (e.g., Circular No. 390/Misc./116/2017-JC). Hence it can be contended that the appeal pending before the appellate authorities can be withdrawn citing the intention to avail the benefit under the scheme.

Once such appeal is withdrawn, the restrictions contained u/s. 125(1)(a) would not apply. The tax dues emanating out of the order would then tantamount to the amount in arrears which can be declared under the scheme.

Restriction given u/s. 125(1)(a) of the Act only debars the persons who have filed an appeal before the appellate forum and such appeal has been heard finally on or before the 30th day of June, 2019 from making a declaration under the scheme.

Hence a person who has filed an appeal on or after 1st July, 2019 can choose to withdraw such appeal and hence file a declaration under the amount in arrears category. Also if such appeal is heard and order is pronounced before the cut-off date for the scheme, declaration can be also made as amount in arrears.

FAQ’s released by the Government on the issue at Q7 says that in cases where appeal is filed on or after 01.07.2019 shall not be eligible to file a declaration under the Scheme. However said FAQ has not considered the aspect of filing a declaration under the amount in arrears category after withdrawal/disposal of the appeal.

Circular No. 1071/4/2019 CX 8 clarifies that the scheme would also cover call book cases. According to the Manual of Office Procedure brought out by the Department of Administrative Reforms and Public Grievances, a call book is required to be maintained by a Department in which a case, which had reached a stage where no action could, or needed to be taken to expedite its disposal for at least 6 months (e.g., cases held up in the law courts), could be transferred with the approval of a competent authority. Cases transferred to the call book are not included in the monthly statement of pending cases. In the context of indirect tax enactments, the Call book cases are those Show Cause Notices, which cannot be adjudicated immediately due to certain specified reasons and adjudication is to be kept in abeyance by transferring such cases to call book. Circular No. 162/73/95- CX.3, dated 14-12-1995 read with Circular Nos. 992/16/2014-CX, dated 26.12.2014 and 1023/11/2016–CX dated 08.04.2016, has specified certain categories of cases which can be transferred to call book (e.g., cases wherein on identical issue the Department has filed appeal before higher appellate authority against the order passed by the lower authority, which was against the Government).

Thus matters under call book are also covered under the scheme and hence the person in question can also opt for the scheme if he finds higher risk of eventual outcome of the dispute.

Sec. 125(1)(b) of the Act debars the person from making a declaration on the matter for which such person has been convicted for any offence punishable under any provisions of the indirect tax enactment. Hence persons convicted for a certain matter cannot overthrow the said conviction by making a declaration under the scheme. It must be noted that cases where only prosecution has been launched but conviction has not happened will not be restricted under the scheme.

The word “offence” has been defined in the Dictionary of Law by L. B. Curzon as that which is equivalent to a crime i.e. an act or omission punishable under criminal law (ref. Derbyshire CC v. Derby [1896] 2 QB 57; Horsfield v. Broan [1932] 1 KB 355).

Sec. 3(38) of the General Clauses Act, 1897 defines the term “offence” to mean any act or omission made punishable by any law for the time being in force.

There is marked distinction between penalty under the law and prosecution. As held by Andhra Pradesh High Court in the case of Thakur V. Hari Prasad v. CIT (1987) 167 ITR 603, penalty proceedings are not criminal proceedings in the strict sense. In a criminal charge, unless the prosecution proves beyond a reasonable doubt the offence committed by the assessee, the delinquent is entitled to the benefit of doubt and thereby goes scot free. The standard of proof for imposition of penalty is not as rigorous as that for prosecution of an offence.

Punishment hence is accorded by the Court of Law and is independent of penalties and confiscation that can be imposed by Excise Authorities through departmental adjudication.

Sec. 9 of the Central Excise Act, 1944 contains provisions related to the offences which are punishable. Punishment is given by way of imprisonment and fine. Similarly section 89 of the Finance Act, 1994 contains provisions related to prosecution of offences under the service tax.

Thus it can be said that mere imposition of penalty on a person on a certain matter in the past would not disentitle him from making a declaration under the scheme.

Close reading of clause (b) will also show that the said restriction applies only in respect of matter for which the person has been convicted for an offence. Hence such person would be able to make a declaration in respect of matters for which he has not been convicted for any offence. As an example let us say that a person has been convicted of an offence of availing and utilising CENVAT credit without actual receipt of taxable service or excisable goods (Sec. 89(1)(b) of FA, 1994). Such person therefore cannot make a declaration with respect to said matter. However such person will be able to make a declaration with respect to other matters.

The said restriction applies across all categories of declaration. Once it is found that the person in question has been convicted for a particular matter in the past, said person cannot make a declaration under the scheme on the same matter even if such matter is pending under the litigation.

Sec. 125(1)(c) of the Act debars the persons who have been issued a show cause notice, under indirect tax enactment and the final hearing has taken place on or before the 30th day of June, 2019 from making a declaration under the litigation category.

Readers may refer to the question related to “final hearing” in the context of appeals for understanding the said term. In the context of show cause notice except situations wherein adjudication order has already been issued on or after 1st July, 2019 having the last hearing taken place on or before 30th June, 2019, the factum of establishing whether final hearing has taken place or not would be required.

CBEC vide Circular No. 1053/2/2017 dt. 10.03.2017 dt. 10.03.2017 has laid down at para 14.10 that the adjudicating authorities have to pass orders within a period of 30 days of conclusion of the hearing barring in exceptional circumstances to be recorded in the file. Hence a clarification is required as to whether the embargo from making the declaration u/s. 125(1)(c) shall apply to situations wherein the said period of 30 days has already passed and order has yet not been passed without recording any exceptional circumstances. The above referred circular only stipulates time limit for passing the order and does not automatically grant a rehearing. Person in such case desiring to make additional submissions or seeking an additional hearing can contend that the final hearing has not taken place.

Even if final hearing pursuant to a show cause notice has happened on or before 30th June, 2019, the dues emanating out of adjudication order passed thereafter can also be declared under the scheme under “amount in arrears” category. Please refer our discussion later on this aspect.

Sec. 125(1)(d) of the Act debars the persons, who have been issued a show cause notice for recovery of an erroneous refund or rejection of refund, from making a declaration under the scheme. Said debarment stems from the fact that the person in question has alleged to have been received an erroneous refund or have made wrong claim of refund and show cause notice is issued seeking the recovery or rejection of the same. If the relief is granted in this regard, it may happen that the persons who would have actually obtained an erroneous refund or refund not supported by law would get enriched at the expense of the Government since such person would have then been not required to pay the partial refund amount or any interest or any penalty in this regard. Moreover, granting of refund requires deeper examination of facts and documents to curb the menace of wrongful and bogus claims.

One may note that there is no debarment (on the ground of unjust enrichment) in situations under amount in arrears category wherein a person has collected the tax but has not paid the same.

Sec. 125(1)(e) of the Act debars the persons, who have been subjected to an enquiry or investigation or audit but the amount of duty involved has not been quantified on or before the 30th day of June, 2019, from making a declaration under the enquiry/investigation/audit category.

Thus only the person who has been subjected to an enquiry or investigation or audit and the amount of duty involved has been quantified on or before the 30th June, 2019 would be eligible to make a declaration under the said category.

The term “enquiry or investigation” has been defined u/s. 121(m) of the Act as follows:

“(m) ‘‘enquiry or investigation’’, under any of the indirect tax enactment, shall include the following actions, namely:— (i) search of premises; (ii) issuance of summons; (iii) requiring the production of accounts, documents or other evidence; (iv) recording of statements;”

Actions such as search of premises, issuance of summons, requiring the production of accounts, documents or other evidence or recording of statements, when undertaken by the department would be considered as a factum for deciding whether the person has been subjected to an enquiry/investigation or not.

The word “audit” has been defined u/s. 121(g) of the Act as under:

“(g) “audit” means any scrutiny, verification and checks carried out under the indirect tax enactment, other than an enquiry or investigation, and will commence when a written intimation from the central excise officer regarding conducting of audit is received;”

Above definition provides that any scrutiny, verification and checks undertaken after a written intimation from the central excise officer regarding conducting of audit is received shall be considered as “audit”.

The word “quantified” has been defined u/s. 121(r) of the Act as under:

“(r) ‘‘quantified”, with its cognate expression, means a written communication of the amount of duty payable under the indirect tax enactment;”

Hence a written communication of the amount of duty payable on or before 30th June, 2019 pursuant to an enquiry/investigation/audit would be considered as “quantified” so as to enable the declaration of the same under the scheme. Also definition of the word “quantified” supra does not provide the person who is supposed to quantify the duty payable. It may hence be also noted that the said quantification need not always be from the department. Even the person in question might have intimated the duty payable on or before 30th June, 2019 and the same would also have to be considered as “quantified”.

Further circular No. 1071/4/2019-CX.8 dt. 27.08.2019 clarifies in this regard at paragraph no. 10(g) that the written communication will include a letter intimating duty demand; or duty liability admitted by the person during enquiry, investigation or audit; or audit report etc.

It may happen that a person has been subjected to an enquiry, investigation or audit and only partial dues have been quantified on or before 30th June, 2019. Said dues could have been quantified by way of a letter written by the person in question accepting the liability. Rest of the dues pursuant to the same enquiry, investigation or audit are quantified on or after 1st July, 2019. In such situation can the person make a declaration pertaining to the partial dues quantified on or before 30th June, 2019?

It may be noted that restriction contained u/s. 125(1)(e) of the Act only provides that it shall apply when the dues have not been quantified on or before 30th June, 2019. Also the definition of “tax dues” u/s. 123(1)(c) in respect of which relief is available under the scheme provides that the same shall mean the amount of duty which has been quantified on or before 30th June, 2019. Hence it can be contended that relief under the scheme shall be available in respect of partial amount of duty which has been quantified on or before 30th June, 2019.

It may happen that a single legal entity would have more than one registration (e.g., two factories). Let us say both the factories have been subjected to an audit on or before 30th June, 2019 but dues have been quantified by such date only with respect to one of the factory. Dues have not been quantified with respect to the other factory.

It may also happen that the factory for which the dues have not been quantified as on 30th June, 2019 has one separate appeal pending. Can the person make a declaration with respect to such dues which are under appeal?

As noted earlier, the restriction u/s. 125 are to be seen qua the case and not qua the person. Hence the declaration can be made with respect to the dues which have been quantified on or before 30th June, 2019 for one of the factory. Also declaration can be made with respect to the dues under appeal (as that is a separate case) even though the factory has been subjected to an audit and the dues have not been quantified on or before 30th June, 2019 pursuant thereto.

If the dues of a person, who has been subjected to an enquiry, investigation or audit, has been quantified, on or before 30th June, 2019 such person can make a declaration under the scheme to the extent of such dues which have been quantified. The issue is whether the person who has been subjected to an enquiry, investigation or audit is eligible to make a voluntary disclosure of the dues not quantified on or before 30th June, 2019 and seek relief under the scheme?

Sec. 125(1)(f) of the Act provides that a person shall not be eligible to make a voluntary disclosure after being subjected to any enquiry or investigation or audit. Hence it appears that except the amount of duty which has been quantified on or before 30th June, 2019, the person cannot make a voluntary disclosure after being subjected to an enquiry, investigation or audit.

Also if such enquiry, investigation or audit is initiated on or after 1st July, 2019 the person will not be able to make a voluntary declaration of the dues subject to the said proceedings. It may however be noted that said restriction would only apply to the dues which pertains to such enquiry or investigation or audit. Other cases (such as appeal pending, etc.) can be declared under the scheme.

It may be noted that the debarment from voluntary disclosure u/s. 125(1)(f) of the Act applies if the person in question is subjected to any enquiry or investigation or audit. Please refer the definitions of the said terms discussed earlier in the context of declaration under the enquiry/investigation/audit category.

Definition of audit u/s. 121(g) of the Act is less complex as it categorically includes only situations wherein written intimation regarding conduct of audit has been received by the person in question.

In the case of Hotel Southson Pvt. Ltd. [2018 (18) G.S.T.L. 24 (Mad.)], it the context of VCES has held as under:

“Once it is shown that an audit has been initiated and it is pending, there is no scope for restricting the sweep of Section 106(2)(b) to an audit in relation to a particular kind of service. If at an audit, the department is able to unearth a service being rendered by the assessee, which has neither been registered nor been assessed to, it is definitely open to the department to require the assessee to pay the service tax and the penalty payable for providing such service. The rigour of such taxing statute cannot be whittled down by the appellant by seeking to invoke so called voluntary compliance that too after the fact that the service has not been registered or has not been taxed was discovered by the department.”

Thus it can be contended that the word “audit” has to be interpreted to cover all the transactions pertaining to the time period for which audit has been initiated. Once audit has been initiated and dues have not been quantified on or before 30th June, 2019 voluntary disclosure pertaining to the time period covered by the audit would not be possible.

Definition of “enquiry or investigation” u/s. 121(m) has been drafted in the context of actions taken by the department which includes search of premises, issuance of summons, requiring production of accounts, documents, other evidence or recording of statements. If any of such actions have been taken, it would mean that the person in question has been subjected to an enquiry or investigation.

Circular No. 1072/05/2019-CX dt. 25.09.2019 at paragraph no. 2(vi) clarifies that the Designated Committee may take a view on merit, taking into account the facts and circumstances, as to whether the debarment u/s. 125(1)(f) would apply or not, in cases where documents like balance sheet, profit and loss account etc. are called for by department while quoting authority of Section 14 of the Central Excise Act, 1944 etc. Circular however does not provide for any factor test to be employed by the designated committee while deciding the case.

An issue arose in the context of VCES in the case of Comm. v. Abhay Cotex Pvt. Ltd.[2019 (22) G.S.T.L. 213 (Tri. - Mumbai) as to whether a letter issued by the Range Superintendent seeking information can be construed as enquiry or investigation or not? It was held (relying on the clarification issued by CBEC) that communications, wherein department has sought information of roving nature from potential taxpayer regarding their business activities without seeking any documents from such person or calling for his presence, while quoting the authority of Section 14 of the Central Excise Act, 1944 and Section 72 of the Finance Act, 1994 and/or Rule 5A of Service Tax Rules, 1994 would not be considered as an investigation so as to debar a person from making a declaration. As the letter of the Range Superintendent was not covered under any of the given provisions (when properly construed), it was held that the benefit of VCES cannot be denied.

Also in the case of LV Construction & Company [2016 (1) TMI 825 (Tri – Mumbai)] it has been held that enquiries of roving nature, even though the communication seeking information quoted Sec. 14 of the Central Excise Act, 1944, would not considered as an enquiry debarring the benefit of VCES. Said decision has also been maintained by Bombay High Court 2017 (351) E.L.T. 94 (Bom.).

Hence an enquiry or investigation without invoking proper legal provisions or of roving nature not seeking proper documents or not calling for statement would not debar the person from making a voluntary disclosure. Also as per the latest circular referred earlier, even the cases where documents are called quoting proper provisions may not cause debarment if under the facts and circumstances the designated committee opines so.

It may also be noted that the definition of “enquiry or investigation” as given u/s. 121(m) refers to issuance of summons as one of the action to show that such enquiry or investigation has been initiated. In the context of VCES, Gujarat High Court in the case of Sweta Sales Corporation v. UOI (2015 (37) S.T.R. 167 (Guj.) held that what is material is the fact that summons initiating enquiry/investigation should have been issued and not the fact that such summons should have been served by a given date.

However Bangalore bench of Tribunal in the case of B.R. Ajit v. CCE 2016 (41) S.T.R. 628 (Tri. - Bang.) again in the context of VCES held that that mere issuance of notice invoking the proceedings (in this case show cause notice was issued) would not be enough to create the embargo. Such notices should have been served by a given date so as to come under the said embargo. Hence the words “issued to a person” was read as “served to the person”.

Thus in the context of present scheme it can be contended that the embargo prohibiting voluntary disclosure would apply only if summons initiating an enquiry/investigation should have been served to the person before the date he makes a declaration under the scheme.

Attention is drawn to the decision in the case of Pearl Buildwell Infrastructure Ltd. v. CCE 2016 (44) S.T.R. 100 (Tri. - Chan.) in the context of VCES wherein it has been held that the debarment of the scheme would not apply if the investigation conducted against the appellant by way of summons issued to the appellant has already been dropped. Hence one can contend that the restriction in making a voluntary disclosure as provided u/s. 125(1)(f)(i) supra would apply only if enquiry or investigation or audit is pending on the date of making the declaration.

Sec. 125(1)(f) of the Act provides that a person shall not be eligible to make a voluntary disclosure having filed a return wherein he has indicated an amount of duty as payable, but has not paid it.

Said restriction has to be read along with Sec. 124(1)(c)(iii) of the Act in the context of relief available under the scheme. This shall facilitate better understanding. Sec. 124(1)(c)(iii) of the Act grants relief in the context of the tax dues relatable to an amount in arrears as reflected in a return filed on or before 30th June, 2019. It may appear that there is a contradiction between the provisions of section 125(1)(f)(ii) and section 124(1)(c)(iii) as the former debars the persons from making a voluntary disclosure but the latter grants relief with respect to amount in arrears.

FAQ’s in this respect at Q13 has clarified that Section 125(1)(f)(ii) is an exception to voluntary disclosure category. In other words, a person having filed a return but has not deposited the duty/tax cannot make a voluntary disclosure in respect of the same since the liability already stands disclosed to the Department. On the other hand, section 124(1)(c)(iii) is a sub-set of the ‘arrears’ category, meaning thereby that in respect of such return a declaration can only be filed under the arrears category. As such, there is no contradiction between the two provisions.

Therefore the person who has return dues pending cannot make a voluntary disclosure. However the person who has filed the returns on or before 30th June, 2019 and declared the dues can seek the relief under the scheme to the extent of dues declared under the amount in arrears category. In other words, persons who have filed returns on or after 1st July, 2019 cannot make a voluntary disclosure and cannot even seek relief under amount in arrears category. Such persons thus instead of filing returns should straight away make voluntary disclosure to seek relief under the scheme.

Sec. 129(2)(c) of the Act permits the authorities to set aside the voluntary declaration even after issuance of discharge certificate if any material particular furnished in the declaration is subsequently found to be false.

Circular No. 1071/4/2019-CX.8 dt. 27.08.2019 in this regard clarifies (at para no. 8) that as there is no way to verify the correctness of voluntary disclosure, a provision is made to reopen such declaration within one year of issue of a discharge certificate, if subsequently any material particular is found to be false.

The declaration can be set aside only if such material fact is found to be false within a period of one year of issue of the discharge certificate. Interesting point to observe here is that there is no separate mechanism prescribed in the Act to inform the declarant about such material fact being found false. The above provision however provides that the proceedings under the applicable indirect tax enactment shall be instituted after setting aside the declaration. Thus it can be contended that such proceedings must be initiated within the one year time limit. In other words show cause notice should be issued within one year. Sec. 129(2)(c) of the Act being a special provision shall override the time limits (3 years or 5 years) as provided under the indirect tax enactment (e.g., Central Excise Act, 1944 or Finance Act, 1994) pertaining to the matter and time period covered in voluntary disclosure.

It may also be noted that the above provision can be invoked only if any “material particular” in the voluntary disclosure is found “false”.

The words “material particular” or “false” has not been defined in the Act. Craig R. Ducat in his book “Constitutional Interpretation” has defined the word “material” as something important or relevant as in a material issue, material fact or material witness. Burton’s Legal Thesaurus (3rd Edition) has defined the word “material” to mean “fundamental”, “vital”, “basic”, “cardinal”, “central”, “crucial”, “decisive”, “essential”, “pivotal”, “indispensable”, “elementary” or “primary”. Said meaning has also been relied by Supreme Court in the case of Virender Nath Gautam v. Satpal Singh (2007) 3 SCC 617. Further the words “material fact” have been defined to mean a fact that is significant or essential to the issue or matter at hand (Black’s Law Dictionary as cited in Ismail Kunju v. Panmana Grama Panchayath AIR 2014 Ker 25). “Material particulars” has thus been defined to mean details in support of material facts (see Virender Nath Gautam v. Satpal Singh (supra)).

The word “false” has been defined by Black’s Law Dictionary (6th Edition) to mean that a thing is “false” when it is done or made with knowledge, actual or constructive, that it is untrue or illegal. Said meaning was relied by the Supreme Court in the case of Commissioner of Sales Tax v. Sanjiv Fabrics (2010) 9 SCC 630.

Declaration cannot be set aside on account of immaterial misstatements. Also declaration cannot be set aside on interpretation issues (such as classification, valuation, etc.) if the declarant has a bona fide view as regards the tax dues declared.

Before we end the discussion on the issue the attention of readers is also drawn to one more aspect. Sec. 129(2)(c) of the Act as discussed above does not provide for an opportunity of being heard when the voluntary declaration is set aside owing to the allegedly material fact being found false. Equity demands that an opportunity should be granted to allow the declarant to make the submissions and denying the same can be contested before the Courts.

Sec. 125(1)(g) of the Act debars the persons, who have filed an application before the Settlement Commission for settlement of a case, from making a declaration under the scheme.

Sections 31, 32 & 32A to 32P of Central Excise Act, 1944 contains provisions related to the settlement commission. Said provisions have also been made applicable to service tax w.e.f. 28th May, 2012.

If a person has filed an application before the Settlement Commission for settlement of a case, such person cannot make a declaration under the scheme for the period and matter covered under the settlement application.

It would also appear that if the person has filed an application in the Settlement Commission in the past and the case has already been settled, such person will not be restricted from making an application under the scheme for any other tax dues. This is because the restriction given u/s 125(1)(g) supra specifically prohibits only those persons who have filed an application in the Settlement Commission for settlement of a case and hence the same should be pending for settlement. The logic seems to prohibit persons who have pending applications so as not to usurp the power of the settlement commission by giving the relief under the scheme.

It may also happen that the application filed before the Settlement Commission may abate due to reasons such as rejection of the application by the Commission or due to order of the Commission not being passed within the prescribed time etc. If such an event has already happened, the person in question is not debarred from making a declaration under the clause under present consideration. Said view has been confirmed by circular No. 1071/4/2019-CX.8 dt. 27.08.2019 at para no. 10(f).

Sec. 125(1)(h) of the Act debars the persons from making a declaration with respect to excisable goods set forth in the Fourth Schedule to the Central Excise Act, 1944.

Fourth Schedule to the Central Excise Act, 1944 covers tobacco and manufactured tobacco substitutes as well as petroleum crude, petroleum gases, petroleum oils and oils obtained from bituminous minerals. For detailed list readers may refer to the concerned schedule.

Clause (h) above restricts the persons from making a declaration with respect to the said goods. The said restrictions applies to the declarations under all the categories (viz. litigation, enquiry/investigation/audit, amount in arrears as well as voluntary disclosure). Declaration can however be made by a person dealing in such goods for other tax disputes. The classic example would be unpaid / disputed liabilities payable under reverse charge such as legal services, GTA service, security services, etc. The manufacturer / dealer in petroleum or tobacco products can go for scheme in respect of their unpaid / disputed reverse charge liabilities.

The declaration under the scheme can also be made under the category of “amount in arrears”. Said term as been defined u/s. 121(c) of the Act as under:

“(c) “amount in arrears” means the amount of duty which is recoverable as arrears of duty under the indirect tax enactment, on account of—

(i) no appeal having been filed by the declarant against an order or an order in appeal before expiry of the period of time for filing appeal; or

(ii) an order in appeal relating to the declarant attaining finality; or

(iii) the declarant having filed a return under the indirect tax enactment on or before the 30th day of June, 2019, wherein he has admitted a tax liability but not paid it;”

Before understanding each of the sub-clauses in details, it is important to know that only the amount of duty which is recoverable can be considered as the amount in arrears. Therefore situations wherein only a notice for undertaking any audit, enquiry or investigation is received or only show cause notice is received would not be considered as “amount in arrears” as no amount of duty is recoverable pursuant to such actions (such dues can be declared under the litigation category or audit/enquiry/investigation category subject to restrictions discussed earlier in the book). Only the amount of duty either confirmed by way of an order-in-original, order-in-appeal or self-admitted dues will be considered as the amount in arrears.

The determination of the “amount in arrears” under sub-clause (i) & (ii) above is not with respect to any cut-off date such as 30th June, 2019. Thus even the dues arising after 30th June, 2019 would qualify as “amount in arrears”.

Now sub-clause (i) in the definition covers a situation wherein an order-in-original or an order-in-appeal has been passed determining the amount of duty which is recoverable and no appeal has been filed before the expiry of the period for filing the appeal.

Plain reading would suggest that to fall under the said sub-clause the declarant needs to show that an order-in-original or an order-in-appeal has been passed and time period for filing the appeal against such order has expired. This would mean that the person does not intend to litigate the matter further. The scheme does not stipulate the date by which the said order, an order-in-original or an order-in-appeal should have been passed/issued/received. Hence it can be contended even an order-in-original or an order-in-appeal received on or after 01st July, 2019 would get the benefit of the scheme provided the time limit for filing the appeal has expired before making a declaration under the scheme.

Sub-clause (ii) covers situation wherein an order in appeal relating to the declarant has attained finality. The term “finality” has not been defined in the Act. However when read with sub-clause (i) as discussed above, it would imply that said sub-clause (ii) covers situation wherein an order in appeal attains finality either if there is no further remedy available in law against such order or the declarant does not intend to file an appeal and hence accepts the order in appeal as final. Hence declaration can be made even in situations wherein time period for filing the appeal against an order-in-appeal has not expired on the date of filing the declaration.

Above views get support from the clarification given at para no. 2(viii) of Circular no. 1072/05/2019-CX dt. 25.09.2019.

Sub-clause (iii) covers situation wherein the declarant having filed a return under the indirect tax enactment on or before the 30th day of June, 2019, wherein he has admitted a tax liability but has not paid the same. Thus the amount of duty admitted in the said returns filed on or before 30th June, 2019 would be considered as amount in arrears.

Definition of “amount in arrears” under sub-clause (i) of Sec. 121(c) of the Act includes the amount of duty recoverable on account of no appeal being filed against an order or order in appeal before the expiry of time period for filing the such appeal. Also the said definition under sub-clause (ii) includes the amount of duty recoverable on account of order-in-appeal attaining finality. As contended before, in the case of order-in-appeal it can be argued that even if the time period for filing the appeal against the order-in-appeal has not expired on the date of filing a declaration, a declaration under the scheme of such amount of duty would imply that the said order-in-appeal has attained finality and hence will be considered as “amount in arrears”. However for the order-in-original only sub-clause (i) is applicable and not sub-clause (ii). Said sub-clause only considers the amount of duty recoverable as amount in arrears if the time period for filing the appeal has expired. Hence we have two situations:

If an order-in-original has been served on 01.08.2019, the time period for filing the appeal would expire after three months (i.e., 30.10.2019) and hence a declaration under the scheme can be made after the said date as amount in arrears.

If an order-in-original is however served on 01.11.2019, the time period for filing the appeal would expire only after the closure of the scheme (last date to make application under the scheme is 31.12.2019). Hence strictly the said amount of duty emanating out of the order-in-original may not be considered as “amount in arrears”.

The term “waiver” has been defined to mean an intentional relinquishment of a known right by an express or implied conduct (see Motilal Padampat Sugar Mills Co. Ltd. v. State of UP (1979) 118 ITR 326 (SC)).

In the case of Gangadhar v. Election Tribunal, Vindhya Pradesh, AIR 1954 VP 44 it has been held as under:

“Waiver is abandonment of a right and is either express or implied from conduct. A person who is entitled to the benefit of a statutory provision may waive it and allow the transaction to proceed as though the provision did not exist.”

Hence it can be contended that the statutory right of an appeal can be waived by the conduct of the person in question. A declaration under the scheme of the dues emanating out of order-in-original, wherein the time period to file an appeal against the said order would not have expired, would imply that the declarant in question has waived his right to file an appeal. Hence said dues become recoverable and has to be regarded as “amount in arrears”.

Above view gets support from the clarification given at para no. 2(viii) of Circular no. 1072/05/2019-CX dt. 25.09.2019. The circular clarifies that if person expressly waives his right to file an appeal by binding declaration, he will be eligible for relief under the “amount in arrears” category of the scheme.

The definition of amount in arrears (other than return dues) does not provide for the date by which the said amounts would stand recoverable. Plain reading suggests that even the dues confirmed on or after 1st July, 2019 can be considered as amount in arrears provided no appeal is filed against such order or is withdrawn (if filed) or such order has attained finality.

The definition of “amount in arrears” u/s. 121(c) of the Act includes the amount of duty which is recoverable on account of declarant having filed a return on or before 30th June, 2019 wherein he has admitted the tax but has not paid it. Hence if a person in question has collected the tax and declared the same in the return filed on or before 30th June, 2019, even such person can seek relief under the scheme.

Therefore it would mean that even though the person has collected let us say Rs. 100 as amount of duty from a customer and declared the same in the return filed as payable, such person now needs to pay only 40% (if the tax dues are Rs. 50 lakhs or less) or 60% (if tax dues are more than Rs. 50 lakhs) of the said amount and keep the balance with him though collected as tax from the customer.

It appears that the principle of unjust enrichment has been given a go-by under the scheme.

As discussed earlier, the relief with respect to amount in arrears can be sought by any person as none of the restrictions covered u/s. 125(1) of the Act are applicable.

The amount in arrears also relates to cases wherein the dues have already been admitted by the declarant (return dues). Hence in such scenario, whether the declarant is required to declare anything per se?

As part of the procedure [see Rule 6(2)], even the amount in arrears needs to be declared under the scheme by way of filing an application to seek the relief.

It may happen that a single case may contain many matters (issues) emanating therefrom. Hence can a declarant file the declaration matter wise? In other words can a declarant make a declaration concerning only some matters in a case (where he sees higher probability of losing) and not all?

Sec. 125(2) of the Act only provides that a declaration shall be made electronically in the manner prescribed. Hence the said provision does not specifically prohibit case-wise or even matter-wise declaration.